ETF Investing in Canada: A Complete Beginner's Guide

Everything you need to know about ETF investing in Canada. Covers all-in-one ETFs, Canadian vs US options, MERs, and portfolio construction.

A data-driven examination of exchange-traded fund investing for Canadians — covering fund selection, portfolio construction, and the fee structures that determine long-term outcomes.

Consider two investors who each start with $50,000 at age 30 and contribute $500 monthly for 30 years, earning identical 7% annual returns before fees. The first holds a Canadian equity mutual fund at the national average MER of 2.0%. The second holds an all-in-one ETF at 0.22%. At age 60, the mutual fund investor has approximately $476,000. The ETF investor has roughly $612,000. The $136,000 gap represents nothing more than the cumulative cost of fees — no difference in skill, no difference in market timing, no difference in discipline. Fees are the single variable within an investor's direct control, and they compound relentlessly.

That arithmetic is the foundation of the ETF revolution in Canada. Over 1,100 exchange-traded funds now trade on Canadian exchanges, and total ETF assets in Canada surpassed $400 billion in 2024. This guide provides the framework for navigating that landscape: which funds warrant your attention, how to structure a portfolio based on empirical evidence, and how to execute purchases through a Canadian brokerage.

How to Buy an ETF in Canada: The Practical Steps

Before examining what ETFs are and why they dominate modern portfolio construction, it is worth establishing that the mechanics are straightforward. The entire process, from opening a brokerage account to owning your first fund, can be completed in under 30 minutes.

Step 1: Select a Discount Brokerage

Two platforms serve the majority of Canadian ETF investors:

Wealthsimple Trade — Commission-free trading on all Canadian and US ETFs and stocks. The platform supports fractional shares and automatic recurring purchases. Currency conversion on US-dollar transactions carries a 1.5% fee, waived for subscribers to the Plus tier ($10/month). Optimal for investors focused on Canadian-listed products.

Questrade — Commission-free ETF purchases ($4.95-$9.95 on sales). A more feature-rich platform with detailed charting, research screeners, and support for Norbert's Gambit currency conversion. Better suited to investors who plan to eventually hold US-listed ETFs.

Interactive Brokers and National Bank Direct Brokerage are also competitive, offering low or zero commissions with more advanced toolsets.

Step 2: Open and Fund a Registered Account

Begin with a TFSA — it offers the most flexibility of any Canadian registered account type. The online application requires your Social Insurance Number, government-issued identification, and banking details. Approval is typically same-day.

Link your chequing account and establish recurring transfers. A biweekly deposit aligned with your pay cycle automates the savings process and eliminates the friction of manual transfers.

Step 3: Select Your ETF

For the first purchase, an all-in-one ETF matched to your risk tolerance is the most evidence-supported choice (see the asset allocation section below). XGRO or VGRO — both holding an 80/20 split of global equities and bonds — represent the default recommendation for investors under 50 with a time horizon exceeding 10 years.

Step 4: Execute the Trade

- Enter the ticker symbol (e.g., XGRO) in your brokerage's search field

- Select "Buy"

- Set a limit order at or marginally above the current ask price

- Calculate shares: divide your investment amount by the per-share price

- Confirm and submit

A limit order is preferable to a market order because it sets a ceiling on the price you will pay. This is particularly relevant for ETFs with lower daily trading volume, where market orders can execute at unfavourable prices.

Step 5: Automate Future Purchases

Wealthsimple supports scheduled recurring investments in specific dollar amounts. Questrade requires manual purchase execution on each contribution date. Regardless of platform, the principle is identical: invest a fixed amount on a fixed schedule, irrespective of market conditions. This dollar-cost averaging approach eliminates the behavioural trap of attempting to time entries.

What Exactly Is an ETF?

An exchange-traded fund pools capital from thousands of investors to purchase a diversified basket of securities — stocks, bonds, commodities, or some combination — and divides ownership into shares that trade on a stock exchange throughout the day. Purchasing a single share of an ETF grants proportional ownership of every underlying holding in the fund.

The closest structural analogy is an index fund formatted as a publicly traded security. Where a traditional mutual fund prices once daily after market close, an ETF's share price fluctuates continuously during trading hours, and you can buy or sell at any point the market is open.

How ETFs Compare to Mutual Funds

| Feature | ETFs | Mutual Funds |

|---|---|---|

| Trading | Real-time on stock exchanges during market hours | Priced once daily after 4:00 PM ET |

| Fees (MER) | 0.05%-0.25% for broad index ETFs | 1.5%-2.5% for actively managed funds |

| Minimum investment | One share (typically $20-$100) | $500-$5,000 minimums are standard |

| Management approach | Predominantly passive index-tracking | Frequently active stock-picking |

| Tax efficiency | Structurally more tax-efficient (in-kind creation/redemption) | Can distribute unexpected capital gains annually |

| Access | Any discount brokerage account | Bank branch, advisor, or fund company |

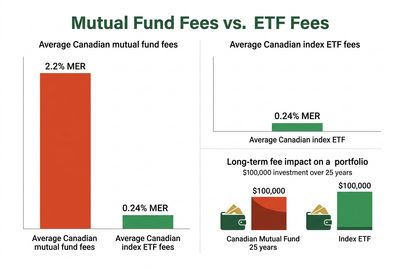

The fee disparity between Canadian mutual funds and ETFs is not marginal. According to Morningstar's Global Investor Experience Study, Canadian mutual fund fees rank among the highest in the developed world. The average equity mutual fund MER of approximately 2.0% is four times the global median. This is not a reflection of superior management — the evidence consistently demonstrates that higher fees correlate with lower net returns, not higher ones.

The fee gap between ETFs and mutual funds in Canada is not a rounding error — it is a structural wealth transfer from investors to fund companies. A couple investing $1,000 per month in mutual funds at 2% versus index ETFs at 0.2% will surrender roughly $200,000 over a 30-year period. That number is not hypothetical. It is basic compound arithmetic, and every Canadian investor should run it for their own portfolio.

The Canadian Case for ETFs

Several characteristics of the Canadian market make ETFs particularly advantageous for domestic investors.

Structural concentration risk. The S&P/TSX Composite Index allocates over 30% to financials, 15% to energy, and 10% to materials. A portfolio limited to Canadian equities is effectively a leveraged bet on commodity prices and bank profitability. All-in-one ETFs like VEQT and XEQT solve this by holding Canadian, US, international developed, and emerging market equities in a single fund — providing genuine global diversification that the TSX alone cannot deliver.

Canadian-specific consideration: Canada represents roughly 3% of global stock market capitalization, yet many Canadian investors hold 50%+ of their equity allocation domestically. This "home bias" concentrates risk in a narrow set of sectors. All-in-one ETFs typically allocate 25-30% to Canada and distribute the remainder globally — a more evidence-based weighting.

Zero-commission infrastructure. The emergence of Wealthsimple Trade and Questrade's free-ETF-purchase model means Canadian investors can deploy capital in amounts as small as $25 without commission drag. This infrastructure did not exist a decade ago and has removed the primary barrier to systematic, small-amount investing.

Registered account synergy. ETFs held within a TFSA grow and compound entirely free of taxation — no capital gains tax, no dividend tax, no tax upon withdrawal. Within an RRSP, the same tax deferral applies, and US-listed ETFs benefit from withholding tax exemptions under the Canada-US tax treaty.

Minimal ongoing management. A single all-in-one ETF rebalances automatically, distributes dividends quarterly, and requires no analysis, monitoring, or decision-making from the investor. The entire annual time commitment is approximately 20 minutes — the time required to review holdings once or twice per year.

ETF Categories Available on Canadian Exchanges

Equity (Stock) ETFs

The primary growth component of any portfolio.

- Broad Canadian market: XIC (S&P/TSX Composite), VCN (FTSE Canada All Cap)

- US market: VFV (S&P 500), VUN (US Total Market)

- International developed: XEF (MSCI EAFE), VIU (FTSE Developed ex-North America)

- Emerging markets: XEC (MSCI Emerging Markets), VEE (FTSE Emerging Markets)

- Sector-focused: TEC (Technology), ZEB (Equal-weight banks), ZRE (REITs)

- Factor-tilted: VDY (High dividend), ZLB (Low volatility)

Fixed Income (Bond) ETFs

Provide portfolio stability, income, and downside protection during equity drawdowns.

- Canadian aggregate: ZAG (BMO Aggregate Bond), VAB (Vanguard Canadian Aggregate)

- Government: ZFL (Long-term government bonds), ZFS (Short-term federal)

- Corporate: ZCS (Short-term corporate), XCB (Canadian corporate bond)

- High yield: XHY (US high-yield, CAD-hedged)

All-in-One (Asset Allocation) ETFs

Complete, globally diversified portfolios in a single ticker. These hold multiple underlying ETFs and rebalance automatically.

- Conservative — 40% equity: VCNS, XCNS

- Balanced — 60% equity: VBAL, XBAL

- Growth — 80% equity: VGRO, XGRO

- All-equity — 100% equity: VEQT, XEQT

Dividend-Focused ETFs

Emphasize companies with established dividend payment histories. For a detailed analysis of dividend strategies, refer to our companion guide on dividend investing in Canada.

International and Emerging Market ETFs

Extend geographic exposure beyond North America into Europe, Asia-Pacific, and developing economies.

- International developed: XEF, VIU

- Emerging markets: XEC, VEE

Canadian ETF Reference Table

| ETF | Provider | Strategy | Holdings | MER | Dist. Yield | Suited For |

|---|---|---|---|---|---|---|

| XEQT | iShares | All-in-one, 100% global equity | 9,000+ stocks | 0.20% | ~1.5% | Maximum long-term growth |

| VEQT | Vanguard | All-in-one, 100% global equity | 13,000+ stocks | 0.24% | ~1.5% | Maximum growth, broader index |

| XGRO | iShares | All-in-one, 80/20 stocks/bonds | 9,000+ stocks + bonds | 0.20% | ~2.0% | Growth with moderate ballast |

| VGRO | Vanguard | All-in-one, 80/20 stocks/bonds | 13,000+ stocks + bonds | 0.24% | ~2.0% | Growth with moderate ballast |

| XBAL | iShares | All-in-one, 60/40 stocks/bonds | 9,000+ stocks + bonds | 0.20% | ~2.2% | Balanced risk-return profile |

| VBAL | Vanguard | All-in-one, 60/40 stocks/bonds | 13,000+ stocks + bonds | 0.24% | ~2.2% | Balanced risk-return profile |

| XIC | iShares | S&P/TSX Composite | 230+ Canadian stocks | 0.06% | ~2.8% | Canadian equity core |

| VFV | Vanguard | S&P 500 (CAD) | 500 US stocks | 0.09% | ~1.2% | US large-cap equity |

| XAW | iShares | Global ex-Canada | 9,000+ stocks | 0.22% | ~1.8% | International complement to XIC |

| VDY | Vanguard | Canadian high dividend | 50+ Canadian stocks | 0.22% | ~4.0% | Income-oriented investors |

| ZAG | BMO | Canadian aggregate bond | 1,400+ bonds | 0.09% | ~3.0% | Portfolio stability, fixed income |

iShares (BlackRock) and Vanguard account for the majority of Canadian ETF assets under management. Their products consistently offer the lowest MERs, deepest liquidity, and tightest bid-ask spreads. BMO rounds out the top three with strong fixed income offerings.

All-in-One ETFs: Evidence-Based Portfolio Construction

Anika (29), a software developer in Ottawa, had accumulated $145,000 across three accounts: a bank RRSP holding two equity mutual funds (average MER 2.15%), a TFSA with a GIC ladder earning 3.8%, and a non-registered account with six individual Canadian bank stocks. Her total annual fee burden was $3,118, and she spent approximately 4 hours monthly monitoring positions and rebalancing. After consolidating everything into XEQT across her TFSA and RRSP at Wealthsimple, her annual fees dropped to $290 — a reduction of $2,828 per year. More significantly, she eliminated all ongoing management. At a projected 7% annual return, the fee savings alone are expected to add approximately $95,000 to her portfolio by age 55.

All-in-one ETFs represent the most significant innovation in Canadian retail investing since the introduction of the TFSA in 2009. Launched by Vanguard in early 2018 and quickly followed by iShares, these products eliminated the two primary barriers to evidence-based investing: the complexity of multi-fund portfolio construction and the discipline required for periodic rebalancing.

Internal Structure of an All-in-One ETF

Each all-in-one ETF is a "fund of funds" that holds a defined allocation across several underlying ETFs. XGRO, for example, holds four iShares component ETFs covering:

- Canadian equities (~25% of equity allocation)

- US equities (~45% of equity allocation)

- International developed equities (~22% of equity allocation)

- Emerging market equities (~8% of equity allocation)

- Canadian, US, and global bonds (20% of total portfolio)

The fund's portfolio managers continuously monitor the allocation and execute trades to maintain the target 80/20 stocks-to-bonds ratio. If equities appreciate and push the allocation to 83/17, the fund redirects incoming cash flows and, if necessary, sells equities to purchase bonds. This rebalancing occurs without any action or decision from the investor.

Selecting the Appropriate Risk Profile

The single decision required is your equity-to-bond ratio, determined by time horizon and genuine risk capacity.

100% equity (VEQT/XEQT): Appropriate for investors with 15+ years before withdrawals who have demonstrated — not merely hypothesized — tolerance for 30-50% drawdowns. Historically the highest-return allocation over multi-decade periods, but the path includes sustained periods of negative returns.

80/20 (VGRO/XGRO): The most widely held all-in-one profile. Suitable for time horizons of 10+ years. The 20% bond allocation historically reduced maximum drawdowns by 4-6 percentage points relative to all-equity portfolios with minimal long-term return sacrifice.

60/40 (VBAL/XBAL): The institutional default allocation for balanced mandates. Appropriate for investors 5-15 years from their goal or those who prioritize capital preservation alongside moderate growth.

40/60 (VCNS/XCNS): Designed for capital preservation. Suitable for investors in or approaching retirement who require portfolio stability above long-term growth.

The Case Against Adding Funds

Complexity without compensation: Research from Vanguard Canada indicates that investors who hold a single all-in-one ETF and contribute systematically achieve outcomes that match or exceed those of investors who construct multi-fund portfolios — primarily because the single-fund approach eliminates rebalancing drift and behavioural trading errors.

Common justifications for adding funds beyond an all-in-one — and why they typically fail to improve outcomes:

- "I want more US exposure." All-in-one funds already allocate 35-45% of equities to US markets. Layering VFV on top is not diversification; it is a concentrated bet on US outperformance continuing indefinitely.

- "I want dividend income." The underlying holdings already include dividend-paying equities across all geographies. Adding a dividend ETF overweights a single factor at the expense of balanced exposure.

- "I can select better sectors." The empirical record is unambiguous: the S&P Indices Versus Active (SPIVA) Canada Scorecard shows that over 95% of Canadian active fund managers underperform their benchmark over 15-year periods.

The one defensible reason to move beyond a single all-in-one fund is withholding tax optimization: holding US-listed ETFs directly in an RRSP avoids a layer of US dividend withholding tax. This produces measurable savings only at portfolio sizes exceeding $200,000 and introduces meaningful complexity in execution and reporting.

Asset Allocation Framework by Risk Profile

Asset allocation — the division between equities and fixed income — determines approximately 90% of a portfolio's return variability over time, according to landmark research by Brinson, Hood, and Beebower. Fund selection, market timing, and trading activity account for the remainder.

Conservative (30-40% Equity)

Profile: Retirees, investors within 5 years of withdrawals, or those for whom a 20% portfolio decline would cause genuine financial hardship.

Historical annualized return: 4-5% Maximum historical drawdown: -15% to -20% ETF implementation: VCNS or XCNS

Balanced (60% Equity)

Profile: Investors 5-15 years from their objective, or those seeking a historically validated middle path between growth and capital preservation.

Historical annualized return: 5-7% Maximum historical drawdown: -25% to -30% ETF implementation: VBAL or XBAL

Growth (80% Equity)

Profile: Investors with 10-20+ year horizons who accept that short-term losses are an inherent characteristic of equity-heavy allocations, not an aberration.

Historical annualized return: 6-8% Maximum historical drawdown: -30% to -40% ETF implementation: VGRO or XGRO

Aggressive (100% Equity)

Profile: Investors with multi-decade time horizons, stable employment income, and a verified ability to maintain contributions during prolonged market declines. The critical qualifier is behavioural: most investors overestimate their risk tolerance until they experience an actual drawdown.

Historical annualized return: 7-9% Maximum historical drawdown: -40% to -50% ETF implementation: VEQT or XEQT

Risk tolerance self-assessment: Visualize your $50,000 portfolio declining to $27,500 over 90 days — and remaining at that level for 18 months. If your instinct is to liquidate, you require more fixed income allocation. If your instinct is to increase your contribution amount, a 100% equity allocation may be appropriate for your temperament.

Canadian-Listed vs. US-Listed ETFs

Canadian investors have access to ETFs on both the TSX (denominated in CAD) and US exchanges such as NYSE and NASDAQ (denominated in USD). The decision between them involves trade-offs across cost, taxation, and operational complexity.

Canadian-Listed ETFs

- Trade in Canadian dollars — zero currency conversion required

- Straightforward Canadian tax reporting (T3/T5 slips issued automatically)

- Eligible for all registered account types (TFSA, RRSP, RESP, FHSA)

- Commission-free at major discount brokerages

Cons:

- Modestly higher MERs than direct US equivalents

- An additional layer of withholding tax on US dividends in all account types except RRSP

- Narrower product selection compared to US exchanges

US-Listed ETFs

- Lower MERs (VTI at 0.03% vs. VUN at 0.17% for equivalent US total market exposure)

- Over 3,000 products with deeper liquidity and tighter spreads

- Eliminates one layer of US dividend withholding tax when held in an RRSP

Cons:

- Currency conversion fees of 0.5%-2.0% unless mitigated via Norbert's Gambit

- T1135 foreign property reporting obligation when total foreign cost base exceeds $100,000

- Potential US estate tax exposure on US-situated assets exceeding $60,000 USD (partially mitigated by the Canada-US tax treaty)

- Wealthsimple applies a 1.5% FX fee on all US-dollar transactions

Practical Thresholds

Portfolios under $100,000: Canadian-listed ETFs are the rational default. The MER differential between a 0.20% Canadian all-in-one and a 0.05% US component portfolio amounts to approximately $75-$150 per year — insufficient to justify the added complexity of currency conversion, multi-fund management, and additional tax reporting.

Portfolios of $100,000-$200,000 and above: The savings from holding US-listed ETFs (VTI, VXUS) directly in an RRSP — primarily the recaptured withholding tax on US dividends — begin to exceed $200-$400 annually. At this scale, learning Norbert's Gambit and managing a multi-ETF portfolio becomes cost-justified.

Canadian tax consideration: The Canada-US tax treaty exempts RRSPs (but not TFSAs) from the 15% US withholding tax on dividends. This means US-listed ETFs held in an RRSP receive full dividend payments, while the same ETFs in a TFSA lose 15% of dividends to unrecoverable withholding. For Canadian-listed ETFs that hold US equities internally, this withholding applies in all account types.

Norbert's Gambit: Institutional-Grade Currency Conversion

Norbert's Gambit exploits the dual-listed nature of certain securities to achieve currency conversion at the interbank rate, bypassing the 1-2% spread charged by banks and brokerages.

- Purchase shares of a dual-listed security on the TSX in Canadian dollars (DLR is purpose-built for this; alternatively, use an interlisted stock such as Royal Bank)

- Contact your brokerage to journal the shares from the Canadian listing (DLR) to the US listing (DLR.U)

- Sell the US-listed shares, receiving US dollars

Settlement requires 2-3 business days. The total cost is limited to the bid-ask spread (typically pennies per share) and any applicable trading commissions. On a $50,000 conversion, this technique saves $500-$1,000 relative to the standard brokerage exchange rate.

Most Canadians do not need US-listed ETFs at all. A single Canadian-listed all-in-one fund gives you global diversification at a cost that is already negligibly low. The investors who benefit from US-listed products are those with large RRSP balances where the withholding tax savings are meaningful. For everyone else, simplicity beats marginal optimization every time.

Rebalancing and Dividend Reinvestment

Rebalancing Mechanics

Investors holding a single all-in-one ETF have no rebalancing obligation — the fund handles this internally. For those managing a multi-ETF portfolio, rebalancing ensures your actual allocation does not drift materially from your target.

Frequency: Semi-annual or annual rebalancing is sufficient. More frequent rebalancing incurs transaction costs and taxable events without improving outcomes.

Threshold approach: Rebalance only when any asset class deviates more than 5 percentage points from its target. This reduces unnecessary trading while maintaining allocation discipline.

Cash-flow rebalancing: Rather than selling overweight positions (which triggers capital gains in non-registered accounts), direct new contributions toward the underweight asset class. This achieves the same result without tax consequences.

DRIP (Dividend Reinvestment Plans)

Most Canadian brokerages offer synthetic DRIP, which automatically reinvests ETF distributions into additional shares.

Wealthsimple: Supports fractional DRIP — every dollar of distributions is reinvested regardless of share price. Enable it on each ETF's detail page.

Questrade: Offers whole-share DRIP only. If your quarterly distribution is $45 and the ETF trades at $50 per share, the DRIP purchases zero shares and the $45 remains as cash. This inefficiency diminishes as position sizes grow and distributions exceed the per-share price.

During the accumulation phase — years or decades before you need to withdraw — DRIP should be enabled on all holdings. The compounding effect of reinvested distributions is a meaningful contributor to long-term returns.

Seven Mistakes That Cost Canadian ETF Investors Real Money

1. Portfolio Sprawl

Holding 8-15 overlapping ETFs does not increase diversification — it increases complexity, raises the probability of rebalancing errors, and often duplicates exposures. A single all-in-one ETF, or a focused portfolio of 3-5 component ETFs for investors with larger balances, is sufficient for any portfolio under $500,000.

2. Performance Chasing

The sector ETF that returned 35% last year frequently underperforms the following year as valuations revert. Thematic and sector funds (cannabis, clean energy, AI, blockchain) exhibit pronounced boom-bust cycles. Core holdings should be broad, market-cap-weighted index ETFs. Speculative sector allocations, if any, should not exceed 5-10% of total portfolio value.

3. Overlooking MERs on Specialty Products

Broad index ETFs charge 0.05%-0.25%. Thematic and actively managed ETFs frequently charge 0.50%-0.80%. On a $200,000 allocation held for 25 years, the difference between a 0.20% and 0.65% MER compounds to approximately $50,000 in additional costs — assuming identical gross returns, which specialty products rarely deliver.

4. Market Timing Attempts

Vanguard's research on lump-sum investing versus dollar-cost averaging demonstrates that immediate deployment of available capital outperforms delayed investment approximately two-thirds of the time across global markets. Holding cash in anticipation of a market correction is, statistically, a negative-expected-value strategy. For investors who find lump-sum deployment psychologically difficult, dollar-cost averaging over 3-6 months is a reasonable compromise — but indefinite waiting is not.

5. US ETFs in a TFSA

US-source dividends paid into a TFSA are subject to an irrecoverable 15% withholding tax. The Canada-US tax treaty's withholding tax exemption applies to RRSPs and RRIFs but explicitly excludes TFSAs. Investors holding US-listed ETFs should place them in registered retirement accounts. Canadian-listed all-in-one ETFs or Canadian equity ETFs are more tax-efficient TFSA holdings.

6. Excessive Trading

ETFs are designed as buy-and-hold instruments. Each sale in a non-registered account is a potential taxable event. More critically, frequent trading is almost always a symptom of emotional decision-making driven by short-term market movements. The evidence-based approach is to establish your allocation, automate contributions, and review the portfolio once or twice annually. The optimal number of trades per year for most investors is 12-24 (monthly or biweekly purchases) plus zero sales.

7. Investing Before Establishing Financial Foundations

An ETF portfolio is a component of a financial plan, not a substitute for one. Before directing capital to markets, confirm that you have established an emergency fund covering 3-6 months of expenses in a high-interest savings account, eliminated all high-interest debt (credit cards at 19-22%, personal lines of credit above 10%), and verified your TFSA and RRSP contribution room through your CRA My Account. Investing while carrying credit card balances at 20%+ is a guaranteed net-negative proposition.

Portfolio Construction by Account Size

A practical framework for evolving your ETF strategy as assets grow:

$0-$25,000 (Foundation Phase)

- Open a TFSA at Wealthsimple or Questrade

- Purchase a single all-in-one ETF (XEQT, VEQT, XGRO, or VGRO based on risk profile)

- Enable DRIP

- Configure automatic recurring deposits

- Review holdings: once per quarter, maximum

$25,000-$100,000 (Accumulation Phase)

- Maintain the single all-in-one ETF strategy

- Maximize TFSA contribution room, then open an RRSP if your marginal tax rate exceeds 30%

- Study asset location principles for future implementation

- Resist the impulse to diversify beyond what your all-in-one fund already provides

$100,000-$250,000 (Optimization Phase)

- Evaluate splitting into component ETFs (XIC + VFV/VUN + XEF + XEC + ZAG) for lower blended MER

- Hold US-listed ETFs in your RRSP to eliminate the withholding tax drag

- Implement Norbert's Gambit for currency conversion

- Open a non-registered account if all registered contribution room is exhausted

$250,000+ (Fine-Tuning Phase)

- Asset location becomes a meaningful return driver — position tax-inefficient holdings (bonds, REITs) in registered accounts

- Consider direct US-listed holdings (VTI, VXUS, BND) in RRSP accounts

- Engage a fee-only financial planner ($1,500-$3,000 for a comprehensive review) for tax and withdrawal planning

- If approaching retirement, begin modelling withdrawal sequencing across account types

At every portfolio size, the principles remain constant: minimize fees, maintain global diversification, align your equity-to-bond ratio with your demonstrated risk tolerance, and avoid the persistent human temptation to predict short-term market direction. The Canadian ETF ecosystem provides institutional-quality investment tools at costs that were inconceivable a generation ago. The determining factor in long-term outcomes is not fund selection — it is the investor's capacity to adhere to a systematic plan through every market environment.

Frequently Asked Questions

Get more free guides

Join thousands of Canadians learning to build wealth the smart way.